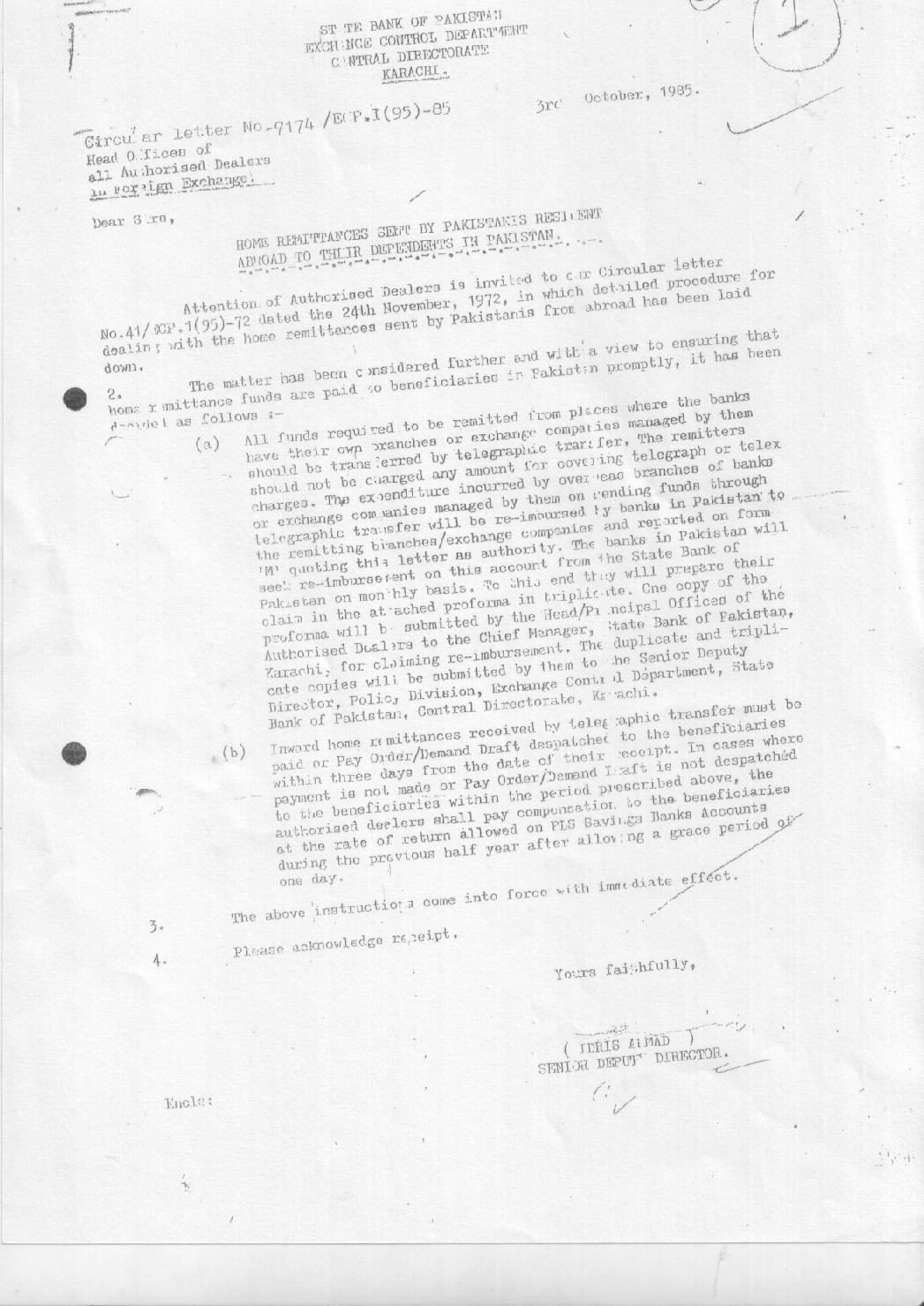

|

The Head/Principal Offices of all

Authorized Dealers in Foreign Exchange

Dear Sirs/Madam,

Home Remittances

Attention of Authorized Dealers is invited to the instructions relating to Home Remittances issued vide FE Circular No. 40 dated July 21, 1998. The said instructions are revised hereunder:

2. With a view to encourage overseas Pakistanis and others to use banking channels for home remittances, and to protect the remitters / beneficiaries from any losses that they may incur due to unwarranted delays in receipts of funds in the beneficiaries’ accounts, it has been decided that the banks shall put in place a mechanism as per PSD Circular No. 02/2009 dated August 22, 2009, within a week which will, interalia, ensure that :

i. In case where the beneficiary is maintaining its account within the same bank, the amount of remittance will be credited to the beneficiary’s account instantly.

ii. In case where the beneficiary is maintaining its account with bank other than the recipient bank, the recipient bank will intimate and give credit of the same to the other bank as per guidelines in PSD Circular No. 02/2009 dated August 22, 2009, however maximum within 24 hours of the receipt of funds. The bank maintaining the account of the beneficiary, after receiving intimation and funds from the recipient bank, will give credit to the beneficiary’s account instantly.

iii. In case where the payment is required to be made through Pay Order/ Demand Draft to the beneficiary, the bank will issue and dispatch the same within the 24 hours of the receipt of funds by the bank.

iv. In case where the banks are offering the facility of cash over the counter to the beneficiary, the banks shall ensure the availability of the funds instantly.

3. In case where the amount of remittance is not credited/ paid to the beneficiary as given in para 2 above, the beneficiary shall be entitled to a return of sixty five (65) paisa per thousand rupees per day for the number of days credit/payment on account of remittance was delayed. The banks are, therefore, directed to ensure that the amount of remittances is credited/ paid to the beneficiary within time frame laid down in para 2 above. In case of delays in the crediting/ making payment of remittance amount, they shall remunerate the beneficiaries at the rate given above.

4. Where a tendency is noted by the State Bank on the part of any bank, either through inspection or on the basis of the pattern of complaints, to delay the credit/ making of payment to the beneficiary’s account, penalties shall be imposed on such banks under the provisions of the Banking Companies Ordinance, 1962. |